Research Piece: Mutual Funds

Too often, sequencers operate under extractive, fee-based models. Mutual ownership offers a better path—where shared responsibility, value circulation, and aligned incentives strengthen the system and serve the community.

This series shares brief case studies of organizations relevant for designing economic mechanisms around ownership of decentralized infrastructure. I intend these posts to be informative, rather than copy-paste recommendations, so I present advantages, disadvantages, and speculations around each model that I learned through my recent research.

Written by Kei Kreutler.

The history of finance can be seen as a history of innovations in pooling capital. While today we might consider index funds commonplace, the mutual ownership structure that enables this emerged from a specific moment in history.

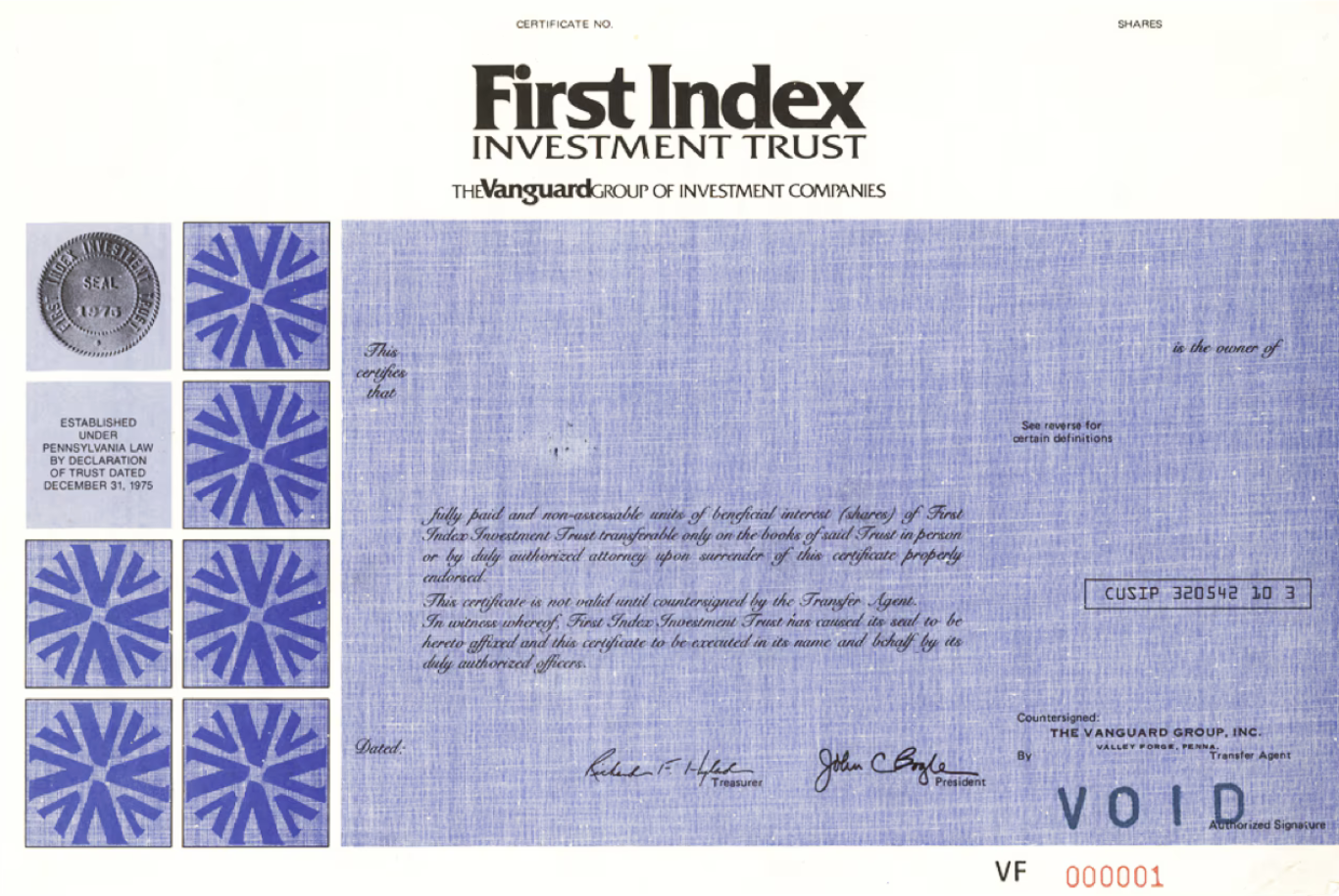

The modern mutual fund industry was transformed by Vanguard’s introduction of a unique ownership structure in 1975. Though mutual funds had existed for decades prior, they typically operated with an external management company extracting significant fees from investors. Vanguard’s innovation was to mutually own the management company itself, ensuring that profits would flow back to fund shareholders rather than external owners.

The Vanguard Group

Vanguard began with a controversial restructuring that made its funds the owners of their management company. This mutual ownership structure meant that Vanguard could operate “at-cost,” passing savings back to investors through lower fees. For example, Vanguard’s first index fund fee was 0.14%, whereas the equity fund category average fee was 1.08% in 1975. The approach was initially met with skepticism from traditional finance, which viewed management companies as essential to the industry. However, as documented in founder John Bogle’s records, every magnitude increase in assets under management allowed fee reductions of 20-30 basis points, creating a compounding feedback loop that persists today.[1]

This structure improved a fundamental principal-agent problem in fund management. By eliminating the profit motive at the management company level, Vanguard aligned the interests of fund operators with fund investors. When combined with index investing, this created a powerful feedback loop: lower costs attracted more assets, which enabled even lower costs through economies of scale. The reduction in fund expenses that followed demonstrated how organizational structure could fundamentally change the economics of financial infrastructure.

Importantly, greater long-term sustainability became possible through reduced conflicts of interest, with governance rights tied to economic participation rather than management status.

Mutual Funds' Relevance for Today

The challenges that Vanguard addressed, aligning the interests of infrastructure operators with users and ensuring efficient operation at scale, parallel many challenges in decentralized finance today.

Though blockchains enable shared, onchain ownership, many projects still struggle with questions around fee structures, governance rights, and operational efficiency that mutual ownership helped address. The move toward mutually-owned infrastructure provides insights for how decentralized services might mature.

Learnings and Examples

The mutual ownership model could inspire how layer 3 networks structure their sequencer relationships and operational costs.

Example Scenario

Consider a layer 3 network called Mutual that reimagines sequencer staking through the lens of mutual fund structures. Rather than treating sequencer stakes as simple deposits, Mutual pools these stakes into an actively managed fund that invests in infrastructure projects vital to the network’s growth.

Sequencers who stake receive shares in this fund proportional to their contribution, creating alignment between sequencer success and ecosystem development. Sequencers can redeem their shares daily based on the fund’s net asset value, but they must maintain a minimum stake to continue participating as sequencers.

```

// SPDX-License-Identifier: UNLICENSED

pragma solidity 0.8.24;

import {IsAllowed} from "src/interfaces/IsAllowed.sol";

/**

* @title MutualFundSequencing

* @dev Validates sequencer membership based on mutual fund shares

*/

contract MutualFundSequencing is IsAllowed {

uint256 public navPerShare; // Updated by fund management

uint256 public constant MIN_STAKE_ETH = 32 ether;

mapping(address => uint256) public shares;

function isAllowed(address proposer) external view override returns (bool) {

uint256 stakeValue = (shares[proposer] * navPerShare) / 1e18;

return stakeValue >= MIN_STAKE_ETH;

}

function stake() external payable {

require(navPerShare > 0, "NAV not initialized");

uint256 newShares = (msg.value * 1e18) / navPerShare;

shares[msg.sender] += newShares;

}

function unstake(uint256 shareAmount) external {

require(shares[msg.sender] >= shareAmount, "Insufficient shares");

uint256 remainingValue = ((shares[msg.sender] - shareAmount) * navPerShare) / 1e18;

require(remainingValue >= MIN_STAKE_ETH || shareAmount == shares[msg.sender], "Must maintain min stake");

uint256 ethValue = (shareAmount * navPerShare) / 1e18;

shares[msg.sender] -= shareAmount;

(bool success,) = msg.sender.call{value: ethValue}("");

require(success, "ETH transfer failed");

}

// Called by fund management to update NAV

function updateNAV(uint256 newNAV) external {

// Add access control in production

navPerShare = newNAV;

}

}

```

Mutual then delegates investment decisions to a council chosen through sequencer governance. This structure transforms sequencer staking from a static security requirement into a dynamic force for infrastructure development, while still ensuring Mutual maintains stable sequencer participation through minimum stake requirements.

In the context of decentralized infrastructure ownership, this model enables sequencer participation to directly fund infrastructure development, giving sequencers exposure to the ecosystem they’re supporting.

[1]: Bogle, 87-91.

Sources

Bogle, John C. Common Sense on Mutual Funds. Hoboken, NJ: Wiley, 1999.

Grohowski, Robert, and Sean Collins. “The Structure and Regulation of Mutual Funds.” In Mutual Funds and Exchange-Traded Funds, edited by H. Kent Baker, Greg Filbeck, and Halil Kiymaz, 65–84. Oxford University Press, 2015. https://doi.org/10.1093/acprof:oso/9780190207434.003.0004.

Investopedia. “Who Owns Vanguard Group?” Accessed January 12, 2025. https://www.investopedia.com/articles/investing/110515/who-are-owners-vanguard-group.asp.

“Vanguard’s History.” Accessed January 12, 2025. https://corporate.vanguard.com/content/corporatesite/us/en/corp/who-we-are/sets-us-apart/our-history.html.